Fréchet distribution

Fréchet

|

Probability density function

|

|

Cumulative distribution function

|

| Parameters |

shape. shape.

(Optionally, two more parameters)

scale (default: scale (default:  ) )

location of minimum (default: location of minimum (default:  ) ) |

| Support |

|

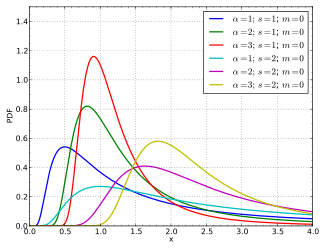

| PDF |

|

| CDF |

|

| Mean |

|

| Median |

![m+{\frac {s}{{\sqrt[ {\alpha }]{\log _{e}(2)}}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/31a72ce4ea6fe77d9c68731c0cafb36bf93dca71) |

| Mode |

|

| Variance |

|

| Skewness |

|

| Ex. kurtosis |

![{\begin{cases}\ -6+{\frac {\Gamma \left(1-{\frac {4}{\alpha }}\right)-4\Gamma \left(1-{\frac {3}{\alpha }}\right)\Gamma \left(1-{\frac {1}{\alpha }}\right)+3\Gamma ^{2}\left(1-{\frac {2}{\alpha }}\right)}{\left[\Gamma \left(1-{\frac {2}{\alpha }}\right)-\Gamma ^{2}\left(1-{\frac {1}{\alpha }}\right)\right]^{2}}}&{\text{for }}\alpha >4\\\ \infty &{\text{otherwise}}\end{cases}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/1f0e101297df7d5cbc11a6a96d305a162371856d) |

| Entropy |

, where , where  is the Euler–Mascheroni constant. is the Euler–Mascheroni constant. |

| MGF |

Note: Moment  exists if exists if

|

| CF |

|

The Fréchet distribution, also known as inverse Weibull distribution, is a special case of the generalized extreme value distribution. It has the cumulative distribution function

where α > 0 is a shape parameter. It can be generalised to include a location parameter m (the minimum) and a scale parameter s > 0 with the cumulative distribution function

Named for Maurice Fréchet who wrote a related paper in 1927, further work was done by Fisher and Tippett in 1928 and by Gumbel in 1958.

The single parameter Fréchet with parameter  has standardized moment

has standardized moment

(with  ) defined only for

) defined only for  :

:

...

Wikipedia